Actual vs Estimates

Vestel Elektronik recorded a net loss of TL7.26bn in 2Q25 vs. a net loss of TL1.30bn in 2Q24 and significantly below both our and market estimate (IS Invest: TL5.06bn; Consensus: TL2.77bn). The weak bottom-line performance was driven by weaker sales volumes and operating margins, particularly in the TV business.

Highlights of the Quarter

Consolidated revenues were at TL34.61bn in 2Q25, down by 18% YoY on the back of decline in domestic and export shipments due to competitive dynamics in major domestic and export markets, as well as softer pricing environment and weak market demand for TV segment. Top-line figure in real TL terms reftlect larger decline as the increase in CPI was greater than USD/TRY exchange rate change in 2Q25. Revenue decrease in USD terms was at 4% in the same period. The household appliances segment posted a 12% YoY revenue decline in 2Q25 while consumer and mobility electronics segment revenues decreased by 29% YoY. In 2Q25 retail TV sales in Türkiye increased by 7% YoY decline and the EU5 market contracted by 9% YoY.

Far below the estimates, 2Q25 EBITDA realized at negative TL536mn, plummeting by 112% YoY in real terms. EBITDA margin came in at -1.5% in 2Q25 vs. 10.4% in 2Q24 due to i) increase in transportation times and costs due to issues surrounding the Red Sea, ii) weak pricing and iii) inflationary impact in TL based costs, labor in particular. TV segment’s margins were particularly weak.

Net financial debt increased by 6% QoQ to TL74.1bn in end-2Q25. However, the net debt/EBITDA ratio rose sharply to 24.1x (vs. 8.7x in 1Q25), mainly due to weak EBITDA performance. Despite improving working capital, FCF was negative at TL1.95bn in 2Q25. The working capital-to-sales ratio declined further to 0.6%, down from 1.9% in the previous quarter and 4.0% at 2024YE. The Company noted that, excluding the impacts of IAS-29, gross and EBITDA margins showed improvement on quarterly basis.

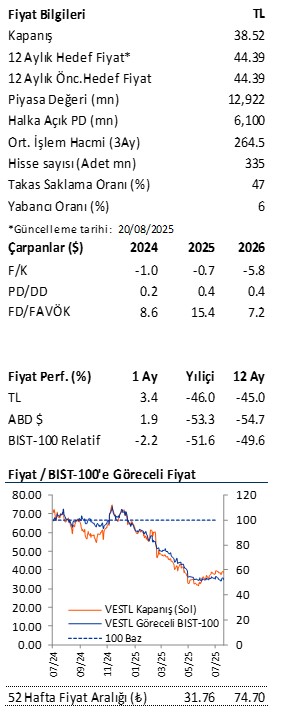

Comment: Market reaction to the weak operating and bottom-line performance should be negative. We continue to expect some improvement in the operating margins going forward on the back of i) gradual recovery in market demand, ii) efficiency program, iii) declining gap between inflation and currency movements, and iv) softening cost pressures. However, we revise down our 2025 projections to 13% real decline in revenues (from 4%) and a 3.8% EBITDA margin (from 7.8)% in 2025. Accordingly, we have cut our TP for VESTL to TL44/share from previous TL57/share. We maintain our HOLD recommendation. We will be monitoring the impact of the efficiency program closely. Tighter monetary stance in domestic market vs. initially expected and potential increase in already intense competition in European market and substantial intercompany receivables are the main risks to our estimates.

Raporu pdf olarak bilgisayarınıza indirmek için tıklayınız.

İlgili hisselerde işlem yapabilmek için lütfen tıklayınız.

Burada yer alan bilgiler İş Yatırım Menkul Değerler A.Ş. tarafından bilgilendirme amacı ile hazırlanmıştır. Yatırım bilgi, yorum ve tavsiyeleri yatırım danışmanlığı kapsamında değildir. Yatırım danışmanlığı hizmeti; aracı kurumlar, portföy yönetim şirketleri, mevduat kabul etmeyen bankalar ile müşteri arasında imzalanacak yatırım danışmanlığı sözleşmesi çerçevesinde sunulmaktadır. Burada yer alan yorum ve tavsiyeler, yorum ve tavsiyede bulunanların kişisel görüşlerine dayanmaktadır. Herhangi bir yatırım aracının alım-satım önerisi ya da getiri vaadi olarak yorumlanmamalıdır. Bu görüşler mali durumunuz ile risk ve getiri tercihlerinize uygun olmayabilir. Bu nedenle, sadece burada yer alan bilgilere dayanarak yatırım kararı verilmesi beklentilerinize uygun sonuçlar doğurmayabilir.

Burada yer alan fiyatlar, veriler ve bilgilerin tam ve doğru olduğu garanti edilemez; içerik, haber verilmeksizin değiştirilebilir. Tüm veriler, İş Yatırım Menkul Değerler A.Ş. tarafından güvenilir olduğuna inanılan kaynaklardan alınmıştır. Bu kaynakların kullanılması nedeni ile ortaya çıkabilecek hatalardan İş Yatırım Menkul Değerler A.Ş. sorumlu değildir.

Bu içeriğe ilişkin tüm telif hakları İş Yatırım Menkul Değerler A.Ş.’ye aittir. Bu içerik, açık iznimiz olmaksızın başkaları tarafından herhangi bir amaçla, kısmen veya tamamen çoğaltılamaz, dağıtılamaz, yayımlanamaz veya değiştirilemez.